Image Sources: LawgicalSearch @Copyright

Introduction

In corporate compliance, definitions are not just a matter of wording — it has legal significance, they dictate what gets prepared, approved, circulated, and filed.

Terms like Annual Report, Financial Statement, and Board’s Report may sound interchangeable, but under the Companies Act, 2013 or the SEBI (Listing Obligation and Disclosure Requirements) Regulations, 2015 (SEBI LODR), they have distinct legal identities and compliance regimes, each serves a distinct legal and regulatory function.

Inaccurate use of these terms (Annual Report, Financial Statement, and Board’s Report) can cause scrutiny from the Ministry of Corporate Affairs (MCA), statutory auditors, or even trigger penal consequences for directors and professionals.

Relevance Under the Companies Act, 2013

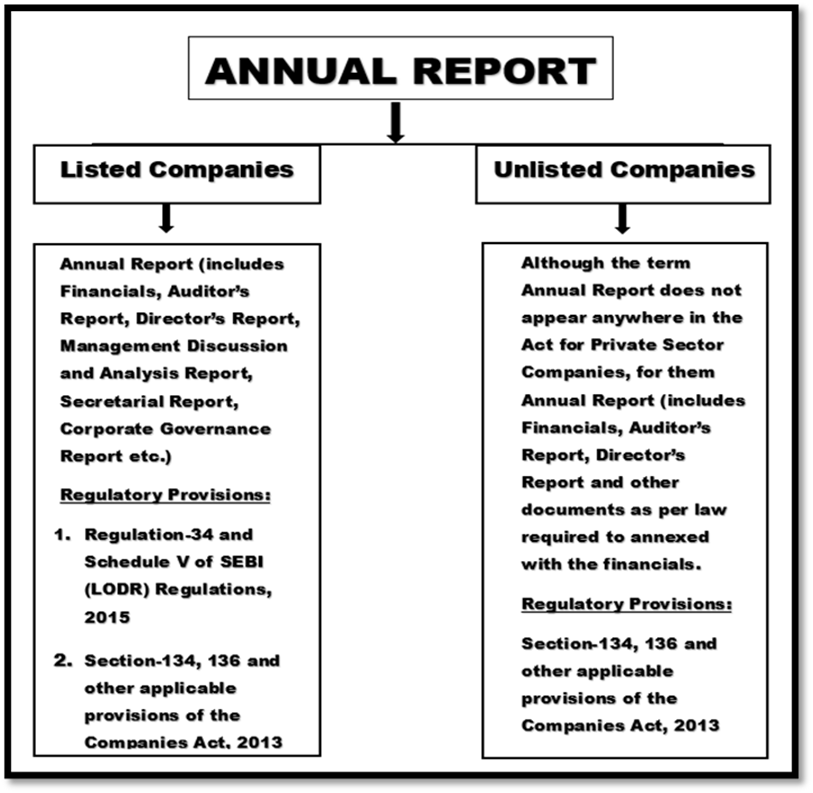

The Companies Act, 2013, along with its allied rules, clearly defines the scope, content, approval process, and filing requirements for Financial Statements and the Board’s Report. While the term Annual Report does not appear anywhere in the Act for Private Sector Companies, it exists as a regulatory requirement under Regulation 34 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 and is applicable only to listed companies.

Under the Companies Act, 2013 “Annual Report” mentioned only for the Government Companies and for Central Government.

In corporate practice, however, many unlisted companies use “Annual Report” informally to describe the complete set of documents presented at the Annual General Meeting — typically comprising the financial statements, consolidated financial statements, the auditor’s report, the Board’s Report, and every other document required by law to be annexed or attached to the financial statements.

Why This Distinction Matters in 2025

With the implementation of MCA V3, data is being validated at the granular level—error-filled or mismatched reporting between financial statements, board reports, and annual filings may now lead to auto-generated show-cause notices.

For instance:

- CSR disclosures under Section 135 must match both the Board Report and the CSR-2 form.

- Financial figures must tally across the Financial Statement, Form AOC-4, and Form MGT-7.

- Omitting any matter required under Rule 8 of the Companies (Accounts) Rules, 2014 in the Board Report, even if the information appears elsewhere in the “Annual Report” — constitutes non-compliance.

The increased compliance-by-design regime requires professionals to understand what exactly each document demands and represents.

Real-world Confusion and Its Impact

Here’s a common scenario: Sometimes a professional uploads only the financials and auditor’s report as part of AOC-4, believing they’ve submitted the “Annual Report.” However, without the Board Report and other document required by law to be annexed or attached to the financial statement like Notice, CSR Report, Secretarial Audit Report (if applicable) etc., the Annual Report is incomplete—and non-compliant.

Such oversight:

- Misleads stakeholders,

- Fails disclosure norms under SEBI (for listed companies),

- And attracts penalties under Sections 134(8) and 137.

In short, understanding the difference between Annual Report, Financial Statement, and Board Report isn’t just good practice—it’s essential for lawful, transparent, and professional corporate conduct in 2025.

Understanding Each Document

- Annual Report – A defined term under Regulation 34 of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (SEBI LODR) for listed companies. Not mentioned in the Companies Act for private/unlisted public companies, though often used in practice to refer to the bundle of documents presented in the AGM.

- Financial Statement – As defined under Section 2(40) of the Companies Act.

- Board’s Report – Required under Section 134, with prescribed contents under Rule 8 of the Companies (Accounts) Rules, 2014.

Annual Report – Meaning

Under the Companies Act, 2013, the term Annual Report does not have any statutory definition for private or unlisted public companies. In its legal sense, Annual Report is used under Regulation 34 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 and is applicable only to listed entities as discussed above.

For listed companies, the Annual Report is a comprehensive disclosure document that must be submitted to the stock exchanges, shared with shareholders and published on the company’s website, containing a wide range of statutory and regulatory reports.

In corporate practice, however, unlisted companies often use “Annual Report” informally to describe the bundle of documents presented at the Annual General Meeting — which typically includes the financial statements, the Board’s Report, the auditor’s report, and other applicable annexures. While this “AGM set” is not legally defined as an Annual Report under the Companies Act, its composition is derived from the combined requirements of:

- Section 134 – Approval and signing of financial statements and Board Report,

- Section 136 – Circulation to members and others,

- Section 137 – Filing of financial statements with ROC via AOC-4,

- Rule 12 of Companies (Accounts) Rules, 2014

In essence, the Annual Report is a packaged disclosure document that includes:

- Financial Statements,

- Auditor’s Report (Auditor’s opinion)

- Board’s Report (Board’s commentary and responsibility)

- CSR Report (CSR and sustainability data (if applicable),

- Secretarial Auditor’s Report

- Other key disclosures as required.

It is laid before the Annual General Meeting (AGM) and shared with members, auditors, debenture trustees, & regulators and published on the Company’s website.

Components of an Annual Report

The contents of an Annual Report vary depending on whether the company is listed (covered under SEBI LODR) or unlisted (private or public).

A. Listed Companies (SEBI LODR – Regulation 34)

For listed entities, the Annual Report is a comprehensive disclosure document mandated under Regulation 34 read with Schedule V of SEBI LODR, and typically includes:

- Corporate Overview – Chairman’s letter, company profile, key milestones

- Notice of AGM – Date, venue, agenda, and resolutions to be passed

- Board’s Report – As per Section 134, Companies Act, 2013

- Auditor’s Report – Statutory audit report under Section 143

- Financial Statements – Standalone and consolidated, along with notes

- Management Discussion & Analysis (MD&A) – Business performance, risks, future outlook

- Corporate Governance Report – As per SEBI LODR requirements

- Business Responsibility & Sustainability Report (BRSR) – For top 1,000 listed entities

- CSR Report – Section 135 compliance.

- Secretarial Audit Report (MR-3).

- All other matters as specified under Regulation-34 read with Schedule V of the SEBI (LODR) Regulations, 2015

B. Unlisted Companies (Section-134, 136 and other applicable provisions of Companies Act, 2013 – Corporate Practice)

For unlisted companies, “Annual Report” is not a statutory term under the Companies Act, 2013. However, in practice, the set of documents placed before the AGM and circulated to members usually includes:

- Notice of AGM – As per Section 101

- Auditor’s Report – Statutory audit report under Section 143

- Financial Statements – Standalone (and consolidated, if applicable) as per Section 2(40) & Section 129

- Board’s Report – As per Section 134 & Rule 8/8A

- CSR Report – If Section 135 applies

- Form AOC-1 – Statement of subsidiaries/associates, if applicable

- Form AOC-2 – Disclosure of related party transactions, if any

- Secretarial Audit Report (MR-3) – If applicable under Rule-9 of Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014

Annual Report Listed vs. Unlisted Companies – A Comparative Analysis

| Component | Listed Companies (SEBI LODR – Reg. 34) | Unlisted Companies (Companies Act, 2013) |

| Legal Status of “Annual Report” | Defined term under SEBI LODR; mandatory for all listed entities | Not defined in the Act; used informally to mean the documents required to be presented at AGM and send to shareholders as per Section-136 of the Act. |

| Governing Law | SEBI LODR Reg. 34 and Schedule V + Companies Act, 2013 | Companies Act, 2013 only |

| Key Sections/Rules | SEBI LODR Reg. 34, Schedule V and Sec. 129, Sec. 134, Sec. 135, Sec. 136, Sec. 137, Rule 8/8A of Companies (Accounts) Rules | Sec. 129, Sec. 134, Sec. 135, Sec. 136, Sec. 137, Rule 8/8A of Companies (Accounts) Rules |

| Typical Contents | Chairman’s Letter MD&ACorporate Governance ReportBRSR (if applicable)Board’s ReportCSR ReportAuditor’s ReportStandalone & Consolidated FSSecretarial Audit Report (MR-3) AGMNotice | Board’s ReportCSR Report (if applicable)Form AOC-1 (if applicable) Form AOC-2 (if applicable)Auditor’s ReportStandalone & Consolidated FS (if applicable)Secretarial Audit Report (if applicable)AGM Notice |

| Circulation | Mandatory to shareholders, stock exchanges, website | Circulated to members, auditors, debenture trustees (if any) – Sec. 136 |

| Presentation | Detailed, investor-focused, with non-financial disclosures | Compliance-focused, containing statutory reports & annexures |

Legal Requirements for Annual Report

Let’s break down the key legal mandates that govern the Annual Report in India:

| Regulation/Section | Mandate | Applicability |

| Regulation-34 read with Schedule V of SEBI (LODR) Regulation, 2015 | Preparation and submission of Annual Report to Stock Exchange, Shared with Shareholders and Publish on website | Listed Companies |

| Regulation-36 SEBI (LODR) Regulation, 2015 | Manner of sending Annual Report to Shareholders | Listed Companies |

| Regulation- 46 SEBI (LODR) Regulation, 2015 | Publishing the complete copy of Annual Report on the Company’s website | Listed Companies |

| Section 134 of the Companies Act, 2013 | Approval and signing of the Financial Statements and Board’s Report, along with prescribed disclosures | All companies |

| Section 136 of the Companies Act, 2013 | Right of members and specified persons to receive the Financial Statements, Board’s Report, and Auditor’s Report before the AGM | All companies |

| Section 137 of the Companies Act, 2013 | Filing of Financial Statements (including the Board’s Report and Auditor’s Report) with the ROC in Form AOC-4 | All companies |

Annual Report Circulation to Stakeholders

- For Listed Companies:

Under Regulation-36 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, a listed entity is required to send a copy of its Annual Report to all shareholders in following manner:

- The soft copy of Annual Report must be sent to all shareholders who have registered their mail with Listed Entity or with any depository at least 21 clear days before the Annual General Meeting (AGM).

- Letter providing the web-link, including the exact path, where complete details of the Annual Report is available to those shareholders who have not registered mail. Timeline: At least 21 clear days before AGM.

- The Annual Report must also be:

- Submitted to the stock exchanges where the company’s securities are listed.

- Placed on the company’s website for public access.

- For Unlisted Companies:

Section 136(1) mandates that the company shall send a physical or electronic copy of the Annual Report (financials + board report + auditor report and other required documents) to:

- All members,

- Debenture trustees (if any),

- All persons entitled to receive notice of general meetings,

- Timeline: At least 21 days before AGM.

Sample Format Table – Annual Report Structure

Below is a practical illustration of how a typical Annual Report is structured for a Unlisted and a Listed Company:

Format: Unlisted Company

| Section | Content |

| Cover Page | Company Name, CIN, Financial Year |

| AGM Notice | Date, time, venue, agenda |

| Director’s Report | As per Sec 134 & Rule 8 |

| Financial Statements | Balance Sheet, P&L, Notes, Cash Flow etc |

| Auditor’s Report | Section 143 statutory audit report |

| Annexure I | Form AOC-1 (if applicable) |

| Annexure II | Form AOC-2 (if applicable) |

| Annexure III | Secretarial Audit Report (if Applicable) |

| Annexure IV | CSR and other applicable documents. |

Format: Listed Company

| Section | Content |

| Chairman’s Letter | Message from Board |

| Business Overview | Company performance summary |

| AGM Notice | Details for shareholders |

| Director’s Report | Sec 134 with Rule 8 & 8A disclosures |

| MD&A | Management Discussion & Analysis |

| Corporate Governance Report | As per SEBI (LODR) Regulations |

| Secretarial Audit Report (MR-3) | As per SEBI (LODR) and Companies Act, 2013 |

| CSR Report | Section 135 |

| Financials (Standalone + Consolidated) | With Auditor’s Reports |

| Annexures | Related Party Transactions, Notes to Account Web links, AOC-1, AOC-2 etc. |

Financial Statement

Meaning – What is a Financial Statement? [Section 2(40)]

As per Section 2(40) of the Companies Act, 2013, “Financial Statement” in relation to a company includes:

(i) a balance sheet as at the end of the financial year;

(ii) a profit and loss account, or in the case of a company carrying on any activity not for profit, an income and expenditure account for the financial year;

(iii) cash flow statement for the financial year (except for One Person Company, small company, and dormant company);

(iv) a statement of changes in equity, if applicable; and

(v) any explanatory note annexed to or forming part of the above.

Thus, a complete Financial Statement includes:

- Balance Sheet

- Profit & Loss Account (or Income & Expenditure)

- Cash Flow Statement (exemptions apply)

- Statement of Changes in Equity (for companies using Ind-AS)

- Notes to Accounts (disclosures & accounting policies)

Legal Basis of Preparation

| Legal Reference | Description |

| Section 129 | Every company shall prepare financial statements that give a true and fair view and comply with accounting standards. |

| Schedule III | Format and disclosure requirements of financial statements. |

| Section 133 | Central Government prescribes accounting standards in consultation with NFRA. |

| Accounting Framework | Either Indian Accounting Standards (Ind AS) or Accounting Standards (AS) depending on the class of company. |

Who Prepares and Approves the Financial Statement?

| Stage | Responsible Party | Legal Provision |

| Preparation | Finance team / CFO | Internal role (notified accounting standards) |

| Approval | Board of Directors | Section 134(1) |

| Signing | As per Section 134(1): |

- Chairperson (if authorised by Board), OR

- Two directors (one of whom must be MD)

AND - CEO (if he is a director)

AND - Company Secretary (if appointed)

AND - CFO (if appointed) | Section 134(1)

Once approved and signed, the financial statements are submitted to auditors for issuing their Independent Auditor’s Report under Section 143.

Filing and Penalty for Non-Filing

Filing Process

- Filed to ROC via Form AOC-4 (within 30 days of AGM).

- If Ind-AS applies, AOC-4 XBRL is mandatory.

- Attachments: Board Report, Auditor’s Report, MGT-9 (or web link), CSR report (if applicable), secretarial audit report, etc.

Penalty for Non-Filing (Section 137)

| Person | Penalty |

| Company | ₹10,000 + ₹100 per day (max ₹2,00,000) |

| Every Officer in Default (Director, CFO, CS, etc.) | ₹10,000 + ₹100/day (max ₹50,000 per officer) |

Note: Even delay of one day triggers penalty. Filing extensions must be backed by valid ROC orders (e.g., GNL-1 condonation in rare cases).

Difference Between Standalone and Consolidated Financial Statements

| Basis | Standalone Financial Statement | Consolidated Financial Statement |

| Definition | Financial position of the individual company only | Financial position of holding company + subsidiaries + associates |

| Legal Requirement | Mandatory for all companies | Mandatory if company has subsidiaries, associates, or joint ventures (Section 129(3)) |

| Scope | Assets, liabilities, income, expenses of the company only | Includes group-level financials: parent + all entities under control |

| Compliance | Schedule III (Division I / II / III) and AS or Ind-AS | Same standards, but with Ind-AS 110 for consolidation |

| Disclosure | No inter-company elimination required | Requires elimination of intra-group transactions |

| Filing | Filed with AOC-4 | Filed as Annexure to AOC-4, with AOC-1 |

AOC-1 must disclose:

- Name of subsidiaries,

- % of ownership,

- Net worth and profit/loss attributable,

- Associate company details.

Note: If a company holds even one subsidiary, it must prepare both standalone and consolidated financials—no exemption, even if the subsidiary is dormant or loss-making.

Board’s Report

Meaning – What is the Board’s Report? [Section 134]

The Board’s Report is a statutory narrative prepared by the Board of Directors under Section 134 of the Companies Act, 2013. It provides:

- An overview of the financial performance,

- Strategic decisions and business direction,

- Updates on corporate governance,

- Key regulatory disclosures, and

- Director’s accountability to the shareholders.

It acts as a bridge between the numbers (in the financial statement) and the context behind those numbers—such as decisions, risks, CSR initiatives, board activities, and more.

Mandatory Contents of Board’s Report

(As per Rule 8 of the Companies (Accounts) Rules, 2014)

Here is a consolidated checklist of mandatory disclosures required in the Board’s Report (for all companies except small companies and OPCs):

| S. No. | Particulars | Legal Source |

| 1 | Extract of Annual Return (MGT-9 or web link to MGT-7) | Sec 92(3) & Rule 12(1) |

| 2 | Number of Board Meetings held | Rule 8(1) |

| 3 | Director’s Responsibility Statement | Sec 134(5) |

| 4 | Details of frauds reported by auditors | Sec 143(12) |

| 5 | Declaration by Independent Directors (if applicable) | Rule 8(5)(iiia) |

| 6 | CSR initiatives and annual report (if Sec 135 applies) | Rule 9 of CSR Rules |

| 7 | Explanation or comments by Board on Auditor’s Qualifications, Reservations or Adverse Remarks | Sec 134(3)(f) |

| 8 | Material changes and commitments affecting financial position after year end | Rule 8(5)(vii) |

| 9 | Conservation of energy, technology absorption, foreign exchange earnings/outgo | Rule 8(3) |

| 10 | Details of subsidiaries, associates, or JVs (in Form AOC-1) | Sec 129(3) |

| 11 | Internal Financial Controls (IFC) – Adequacy & effectiveness | Sec 134(5)(e) |

| 12 | Annual evaluation of Board and committees | Rule 8(4) |

| 13 | Remuneration policy & details of managerial remuneration | Sec 197 read with Rule 5 |

| 14 | Details of significant and material orders passed by regulators/courts | Rule 8(5)(viii) |

Additional Disclosures for Listed Companies – Rule 8A

Listed companies must additionally include the following:

| Disclosure | |

| Performance and financial position of subsidiaries, associates, JVs | |

| Change in nature of business | |

| Details of directors/key managerial appointments/resignations | |

| Formal annual evaluation framework | |

| Board-level committees and their activities | |

| Details of sexual harassment cases under POSH (where applicable) |

Legal Requirements – Board Report Compliance

| Provision | Requirement |

| Section 134(1) | Board must attach its report to the financial statement laid before the AGM |

| Section 134(6) | Board’s Report must be approved by Board and signed by: |

- Chairperson (if authorised),

- Else, two directors, including one MD, where there is one.

- Timeline Attached to Financials → Circulated with Annual Report → Filed via AOC-4

Small Companies / OPCs Allowed abridged Board’s Report under Rule 8A(1) of Companies (Accounts) Rules, 2014

Suggested Format – Board’s Report (Infographic Table)

Here’s a simplified and visual-friendly sample structure of a typical Board’s Report for clarity:

| Section | Contents |

| Introduction | Overview of company’s performance, business context |

| Financial Highlights | Summary of financial results – turnover, PAT, net worth |

| Operational Review | Key achievements, milestones, expansion, challenges |

| Board Meetings | Dates and attendance record |

| Director’s Responsibility Statement | Assurance on preparation of FS, compliance, IFCs |

| CSR Report (if applicable) | Activities, expenditure, impact |

| Conservation of Energy & Tech Absorption | Green practices, R&D, innovations |

| Related Party Transactions | Disclosure as per Section 188 and AS-18 / Ind-AS 24 |

| Subsidiaries & Associates | Performance summary + AOC-1 reference |

| Risk Management & IFCs | How risks are identified, mitigated |

| Comments on Auditor’s Report | Clarification on any qualifications |

| Acknowledgements | Thanks to stakeholders, employees, etc. |

Note: The Board’s Report is where compliance meets communication. While it must meet legal mandates, it’s also the place where companies can build trust by showing transparency, ethics, and vision.

Comparison Table – Annual Report vs. Financial Statement vs. Board Report

| Feature | Annual Report | Financial Statement | Board Report |

| Meaning | A comprehensive document presented to stakeholders containing financials, reports, and disclosures | The core set of financial documents that present the financial health and performance of the company | A narrative report by the Board explaining performance, strategy, governance, and statutory disclosures |

| Legal Reference | Regulation-34 and Schedule V of the SEBI (LODR) and Sections 134, 136, 137 of the Companies Act, 2013 | Section 129 and Section 2(40) of the Companies Act, 2013 | Section 134(3) and Rule 8 of the Companies (Accounts) Rules, 2014 |

| Filing Form | Submitted to Stock Exchange, Shared with members and publish on Company’s website. | Included in AOC-4 as PDF/XBRL (if applicable) | Part of Annual Report, attached with AOC-4 |

| Due Date | At least 21 days before the Annual General Meeting. | Within 30 days of AGM | Same due date as Annual Report – part of AOC-4 |

| Format Defined | No specific format, but must include specific disclosures as per Companies Act | Schedule III (Division I / II / III) format, depending on company type | No rigid format – must contain disclosures as per Rule 8 / 8A |

Practical Significance for Professionals

Importance of Accuracy in Board’s Report Narrative

The Board’s Report is not just ceremonial. It’s your signed declaration to MCA and shareholders. As per Section 134 of Companies Act, 2013, this report must:

- Be factually consistent with auditor’s report, AOC-4, CSR-2, MGT-7/7A

- Carry a clear statement of compliance under 134(3)(f) and (5)

- Include disclosures like:

- State of the company’s affairs

- Amounts proposed to be carried to reserves

- Dividends (if any)

- CSR activity report

- Frauds, directors’ responsibility statement, etc.

A copy-paste approach is dangerous. Directors signing off an inaccurate report can face penal actions under Section 134(8) – up to ₹50,000 fine or imprisonment in severe cases.

Practical Compliance Checklist for CSs, CAs & Directors (FY 2024–25 onwards)

Here’s a practical, V3-compliant checklist your team should use before filing:

| Category | Compliance Point | Cross-check with | Responsible Officer |

| Board’s Report | Consistency of narrative with MGT-7, AOC-4 | All statutory filings | CS, Director |

| Dates | AGM, Board Meeting, Signing date sequence | MGT-7, AOC-4 | CS |

| Financials | Match profit, depreciation, tax, dividend info | FS, Notes, AOC-4 | CA, CS |

| Auditor Remarks | Auditor’s observations & CARO applicability | Board’s Report, Sec 134(3)(f) | CA |

| Director Disclosures | DIN status, resignation date, meetings attended | MGT-7, DIR-12 | CS |

| CSR | Match Board Report narrative with CSR-2 | CSR-2, Sec 135(4) | CS, CSR Committee |

| Fraud Reporting | Any fraud under Sec 143(12) mentioned? | Audit Report vs. Board Report | CA, CS |

| Certification | Ensure MD/Director & CS digitally signed the forms | AOC-4, MGT-7 | CS, Director |

| Attachments | Ensure all attachments are legible PDFs, signed | Board’s Report, FS, Auditors Report | CS, CA |

| XBRL Filing | Required for certain companies under Rule 12 of Companies (Accounts) Rules, 2014 | AOC-4 XBRL | CA/CS |

Sources for Red Flags & Checklist

- Companies Act, 2013 – Sections 92, 129, 134, 135, 173, 143

- Rules under Companies (Accounts), (Management & Administration), and (CSR Policy) Rules, 2014

- MCA V3 Filing Guides and FAQs

- MCA Notifications dated 14.08.2019, 23.01.2023, 21.02.2023

- ICSI & ICAI Guidance Notes (2022–24 Editions)

- Field observations from CSs and tax professionals (via Lawgical Search network)

Final Conclusion – The Compliance Trinity

The Annual Report, Financial Statement, and Board’s Report are three pillars of statutory disclosure — each with its own legal DNA, audience, and filing mandate under the Companies Act, 2013.

- The Financial Statement speaks in numbers.

- The Board’s Report speaks in narrative and it is a part of Annual Report

- The Annual Report speaks as the complete voice of the company.

Treating them as one will invite MCA scrutiny; treating them distinctly will earn you shareholder trust and regulatory peace of mind.

Annexures

To ensure absolute clarity for CS professionals, compliance officers, auditors, and directors, we’re attaching sample formats and comparative tables below. These are strictly for educational and illustrative purposes. Always follow the latest MCA, ICAI, and SEBI circulars, and notify changes under secretarial standards.

Sample Format: Annual Report (Private Limited Company)

(Abridged Structure – Tailor as per company size and statutory requirement)

markdown

ABC PRIVATE LIMITED

(CIN: U12345DL2021PTC000111)

Registered Office: XYZ Complex, New Delhi, India

Email: info@abc.com | Website: www.abc.com

**ANNUAL REPORT**

For the Financial Year Ended 31st March, 2025

INDEX

1. Company Profile

2. Notice of AGM

3. Board’s Report

4. Management Discussion and Analysis (If applicable)

5. Financial Statements

– Balance Sheet

– Profit & Loss Account

– Cash Flow Statement

– Notes to Accounts

6. Auditors’ Report

7. Corporate Governance Report (if applicable)

8. Secretarial Audit Report (if applicable)

9. Other annexures

Issued by: For ABC Private Limited Sd/-

[Name of Director]

DIN: xxxxxxx

Date: 10th August, 2025

Sample Format: Board’s Report (as per Section 134)

BOARD’S REPORT

To,

The Members,

ABC Private Limited,

Your Directors have pleasure in presenting the Board’s Report for the financial year ended 31st March 2025.

1. Financial Results (in ₹ lakhs)

2. State of Company’s Affairs

3. Dividend Declaration

4. Transfer to Reserves

5. Change in Share Capital or Directors

6. Extract of Annual Return (MGT-9 or web-link)

7. Meetings of Board

8. Directors’ Responsibility Statement

9. Auditors and Audit Report

10. Particulars of Employees (Rule 5)

11. Secretarial Audit Report (if applicable)

12. Internal Financial Controls

13. Material Changes after Financial Year

14. Risk Management Policy

15. CSR (if applicable)

16. Related Party Transactions

17. Details under Sexual Harassment Act

18. Other disclosures as applicable

Signed for and on behalf of the Board of Directors

Sd/-

[Name] – Director

DIN: xxxxxxx

Date: 10th August, 2025

Format Table: AOC-4 Content Mapping

(Understand which document supports which field in AOC-4)

| Sl. No. | AOC-4 Field | Source Document | Remarks |

| 1 | Financial Position | Balance Sheet | Part of Financial Statements |

| 2 | Profitability | Profit & Loss A/c | Mandatory upload |

| 3 | Cash Flow Statement | Cash Flow | For companies under Ind AS |

| 4 | Directors’ Report | Board’s Report | Attach separately |

| 5 | Auditors’ Report | Statutory Auditor’s Report | Attach with financials |

| 6 | Corporate Social Responsibility Report | CSR Annexure | Applicable if CSR under Section 135 |

| 7 | AOC-2 – RPT disclosure | Annexure to Board’s Report | Related Party Transactions |

| 8 | Web Link | Board’s Report | Mandatory under Section 92 |

| 9 | Secretarial Audit Report | MR-3 | Only for listed / big companies |

| 10 | Notes to Accounts | Financial Statements | Critical component – discloses accounting policies |

Note: Always cross-verify formats with the latest MCA notifications, ICAI and ICSI guidance notes, and check the applicability of Ind AS, CARO, and Schedule III Part II amendments.

Frequently Asked Questions (FAQs)

Is Financial Statement same as Annual Report?

No, not exactly.

A Financial Statement refers specifically to documents like the Balance Sheet, Profit & Loss Account, Cash Flow Statement, Statement of Changes in Equity, and Notes to Accounts, prepared under Section 129 of the Companies Act, 2013.

Whereas, an Annual Report is a broader document. It includes the Financial Statement, Board’s Report, Auditor’s Report, Corporate Governance Report (if applicable), and other statutory disclosures. Think of the Annual Report as the full story, and Financial Statements as just one (important) chapter.

Can a Private Company skip the Board’s Report?

No. Every company (except One Person Company) is mandatorily required to prepare a Board’s Report under Section 134 of the Companies Act, 2013, irrespective of whether it is a private or public company.

However, small companies and OPCs can use a shorter format of Board’s Report as prescribed under Rule 8A of the Companies (Accounts) Rules, 2014 (amended).

Who signs the Annual Report?

The Annual Report is signed by:

- Financial Statements: Signed by

- Chairperson (if authorised by the Board), or

- At least two directors, one of whom must be the MD or Whole-time Director, and

- CFO and Company Secretary, if they are appointed

(Section 134(1) of the Companies Act)

- Board’s Report: Signed by

- Chairperson (if authorised), or

- Two directors, one of whom must be the MD or Whole-time Director

The signing must be done before filing with the ROC in Form AOC-4.

What is the filing due date for AOC-4?

The due date for filing AOC-4 (Financial Statements) with the ROC is:

Within 30 days of the Annual General Meeting (AGM)

- For companies required to hold AGM → Within 30 days of AGM

- For companies not required to hold AGM (e.g., OPC) → Within 30 days from the date when AGM should have been held, usually 30 September

Late filing penalty: ₹100 per day of default under Section 137(3)

Is MGT-9 still mandatory?

No, not for most companies.

As per the Companies (Amendment) Act, 2017, the requirement to attach MGT-9 with the Board’s Report was omitted.

Now, companies must only mention the web-link of the extract of MGT-9 (Shareholding Pattern) in the Board’s Report if they have a website.

For companies without a website, MGT-9 may still be annexed.

Refer: Rule 12(1) of Companies (Management and Administration) Rules, 2014 and MCA General Circulars

Legal References

To navigate through the compliance maze of Annual Reports, Financial Statements, and Board’s Reports, you must understand the legal backbone that supports them. Below are the key Sections, Rules, and MCA Circulars that you should bookmark, study, and refer to during audits, Board meetings, and compliance filings.

Companies Act, 2013 – Key Sections

| Section | Title | Relevance |

| Section 2(40) | Definition of Financial Statement | Sets the legal definition of what constitutes a Financial Statement under the Act. |

| Section 129 | Financial Statement | Lays down preparation, true and fair view, and compliance with Accounting Standards (AS or Ind AS). |

| Section 134 | Financial Statement, Board’s Report, etc. | Governs Board’s Report, signing of financials, disclosures, and Director’s Responsibility Statement. |

| Section 136 | Right of Member to Copy | Deals with circulation and uploading of Financial Statement and Board Report on the website. |

| Section 137 | Filing with the Registrar | Governs e-filing of Financial Statements and Board’s Report using Form AOC-4. |

Companies (Accounts) Rules, 2014

| Rule | Summary |

| Rule 8 | Applicable to all companies (except OPC/Small Co) – prescribes content of Board’s Report including CSR, Loans & Guarantees, Related Party Transactions, etc. |

| Rule 8A | Specific format for Board’s Report for One Person Company (OPC) and Small Companies – much simpler and shorter. |

| Rule 12 | Filing of financial statements with ROC in Form AOC-4 or AOC-4 XBRL, as applicable. |

NOTE: Always check if you fall under XBRL filing applicability – typically listed companies and those meeting threshold limits.

Key MCA Circulars

Below are some important MCA Circulars related to Annual Reports, Board Reports, and Financial Statements:

| Circular No. | Date | Summary | Link |

| General Circular No. 22/2020 | 15.06.2020 | Relaxation on dispatch of physical copies of Annual Reports during COVID-19. | View Circular |

| General Circular No. 10/2021 | 23.06.2021 | Extension for holding AGMs and Board approvals in electronic mode. | View Circular |

| General Circular No. 9/2023 | 25.08.2023 | Updated XBRL filing requirements and changes in AOC-4 format. | View Circular |

These circulars reflect evolving compliance flexibility and digital transformation pushed by MCA under MCA21 V3.

Written by Mahboob Gaddi and Farman Ahmad | Founders, Lawgical Search